Aha — no sooner do I suggest that the craziness associated with discussions of international money has now shifted to money in general than I see Steve Pearlstein writing a column about global economics that I agree with halfway through, but that veers off into a misplaced focus on the international role of the dollar as the key concern. Now, Pearlstein isn’t crazy the way the goldbugs are — but he does seem to share the common tendency to exaggerate the importance of owning a global currency.

By the way, this is home turf for me; I’ve been writing about these issues for a long time (pdf). And one of the odd things about international money is that the more you know about it, the less important you tend to think it is: lay observers think it’s huge, economists who don’t specialize in international macro think it’s pretty big, actual researchers on international monetary issues disagree about exactly how important it is, but by and large they don’t think it’s all that important.

So, what does America gain from the dollar’s special status? One clear gain is that foreigners are holding a lot of pieces of green paper with dead presidents on them — maybe $500 billion worth. That’s in effect a zero-interest loan; in normal times, when short-term interest rates are 4 or 5 percent, it’s worth something like $25 billion a year. Nice, but not a big deal in a $15 trillion economy.

Then come the more dubious parts.

It’s often asserted that it’s only because of the dollar’s special status that America can run persistent trade deficits. But that’s just not true: other countries whose currencies have no special role can do the same, and have.

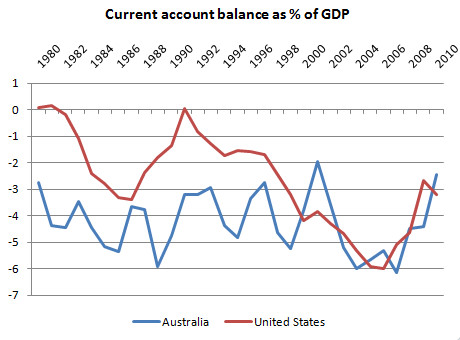

IMF WEO database

IMF WEO database Still, it could be that purchases of Treasuries by foreign central banks keep the dollar stronger and interest rates lower than they would otherwise be. The way to think about this is that Chinese reserve accumulation (say) is a sterilized intervention in the dollar [i.e., one that isn’t allowed to affect the money supply]. In general, we tend to think that sterilized intervention is only modestly effective, because it tends to be offset by private capital moving the other way. But maybe there’s something there.

It’s really hard, though, to see how the benefits of the dollar’s reserve status could be more than a fraction of a percent of GDP. It’s not a trivial issue, but it’s not among the things that should be a key driver of economic concern.